In the summer of 2014, Puzz had another puzzle to solve. From March to July, the frequency with which an IEX customer could have gotten a better price less than 10 milliseconds after a trade posted rose from about 3 percent to as much as 10 percent. This wasn’t meant to happen. IEX was supposed to protect investors from what’s known as stale quote arbitrage; that’s when a high-frequency trader takes advantage of milliseconds-long delays in how markets update prices to reflect movements on other exchanges. These tiny delays allow high-speed traders to see a price fluctuation on one exchange and then quickly send an order to another market—often a dark pool—that it knows updates its prices more slowly, hoping to pick off the orders resting there at stale prices. It’s a bit like betting on yesterday’s horse race against someone who doesn’t know the result.

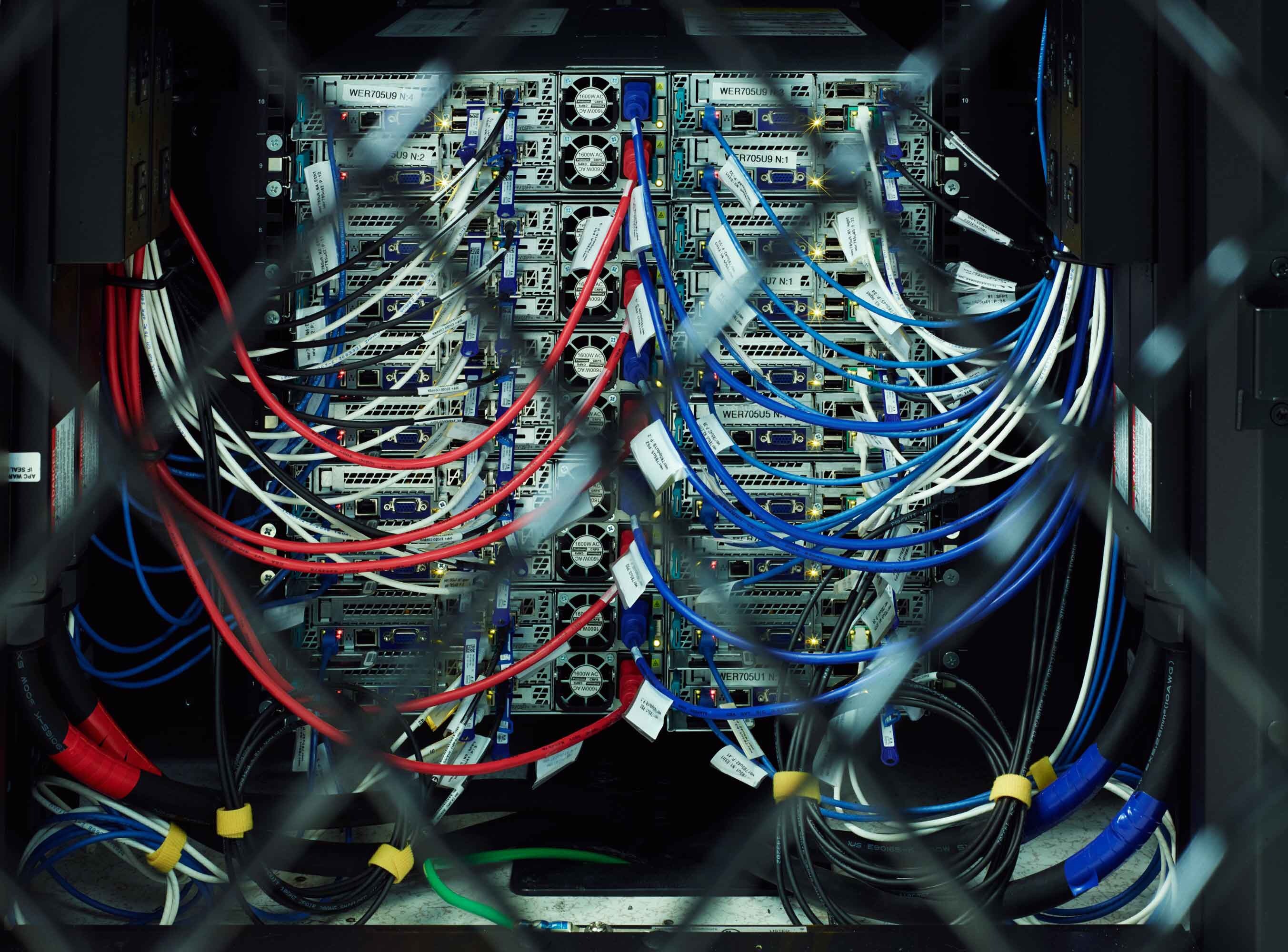

IEX prevents stale quote arbitrage with its “magic shoe box,” a metal container in its data center in Weehawken, New Jersey. Crammed into it are 38 miles (61 kilometers) of coiled fiber-optic wire, creating IEX’s speed bump of 350 microseconds (about one one-thousandth of the time it takes to blink). The idea of countering super-fast traders by creating a slower market might seem like a paradox. It’s not. IEX uses the same high-speed data feeds as HFT firms do to monitor other exchanges for price changes. But because IEX didn’t want to be in a technological arms race with the high-frequency traders to process this information faster than they do, it uses the speed bump to slow down all new orders—just enough to ensure IEX has time to update its prices to reflect any movements on public exchanges. This prevents orders on IEX from being traded against at stale prices.

So how, Aisen wondered, could HFT firms be picking off IEX orders despite the magic shoe box? It didn’t take Puzz long to solve the riddle. He discovered that some HFT algorithms could predict price changes—like surfers sitting out past the break, scanning the swell for their next ride—and target orders before the magic shoe box’s speed bump could protect them.